LEARN FROM HISTORY—OR REPEAT IT

Discover the Four Vital Decades That Defined U.S. Mortgage Securitization

In The Evolution of U.S. Mortgage Securities 1970–2010: Four Decades of Innovation, fintech entrepreneur Michael Youngblood applies his extensive experience in U.S. housing and mortgage markets to supply an essential history of the forty critical years when residential mortgage securitization underwent a heated laboratory of creativity.

Through exhaustive research and detailed accounts, Youngblood illustrates how fragmented, local lending evolved into a vast, open marketplace by solving concrete problems: standardizing loans, spreading risk, and equalizing credit access. Beginning with FHA insurance and the first Ginnie Mae pass-through, Youngblood charts the build-out of agency programs, non-agency conduits, and multiclass CMOs/REMICs, showing how each product tackled funding mismatches, prepayment, and credit risk.

INSIGHTS

We cannot fully understand and appreciate the pros and cons of any product in the universe of U.S. residential mortgage securities unless we also know why that product was developed, including the historical circumstances that led to its development and the problems it was designed to solve. Finally, and perhaps most importantly, as we will see by the end of this book, the global financial crisis of 2007–2009 was a prime example of repeating history’s mistakes by those who had failed to learn from them. By 2000, there was ample and recent historical evidence that the non-agency mortgage securities market had an Achilles’ heel: Companies depended for their very existence on easy access to short-term financing, and once it dried up, the market would collapse. But due to unwarranted optimism that likely sprang from willful historical ignorance, market participants set in motion the same pattern of events that occurred in the late 1990s―with far worse results.

The Evolution of U.S. Mortgage Securities gives novel insights into the history of U.S. residential mortgage securities, including the following:

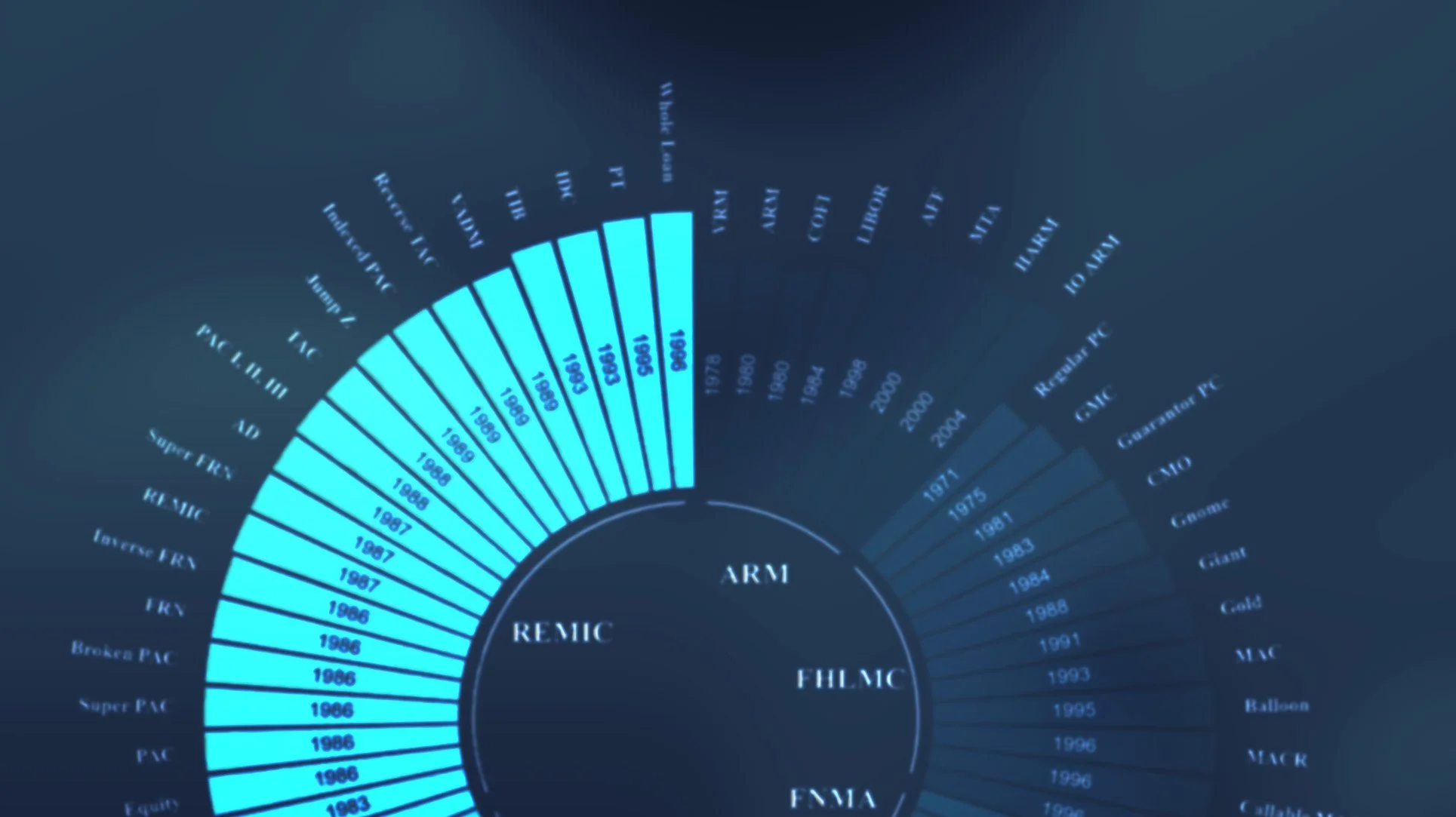

1: The most important events internal to the U.S. mortgage securities market

The issuance of the first Ginnie Mae pass-through certificates (1970), which were the archetype of all subsequent mortgage securities.

The issuance of the first non-agency pass-through securities (1976).

The issuance of the first guarantor agency pass-through securities (1981).

The issuance of the first multiclass mortgage securities (CMO and REMIC, 1983 and 1987, respectively)

The issuance of the first planned amortization class (PAC, 1986)

2: The most important events external to the U.S. mortgage securities market

The passage of the National Housing Act of 1934 (Pub. L. [Public Law] 73-479), which created the Federal Housing Administration and authorized insurance of single-family and project mortgage loans.

The passage of the Housing and Urban Development Act of 1968 (Pub. L. No. 90-448), which created Ginnie Mae and privatized Fannie Mae.

The passage of the Emergency Home Finance Act of 1970 (Pub. L. No. 91-351), which created Freddie Mac.

The radical reform of monetary policy under the Volcker Federal Reserve (1979).

The creation of the REMIC provisions of the Tax Reform Act of 1986 (Pub. L. No. 99-514), which established the federal income tax treatment of multiclass securities and enabled issuance as asset sales or debt.

3: The most important mortgage securities products

Federal Housing Administration insurance of mortgage loans (1934), which established a paradigm for Freddie Mac and Fannie Mae insurance of conventional mortgage loans.

The Ginnie Mae pass-through security (1970), which was the archetype of all subsequent mortgage securities.

The mortgage conduit (1978), which enabled issuance of non-agency mortgage securities by nontraditional lenders.

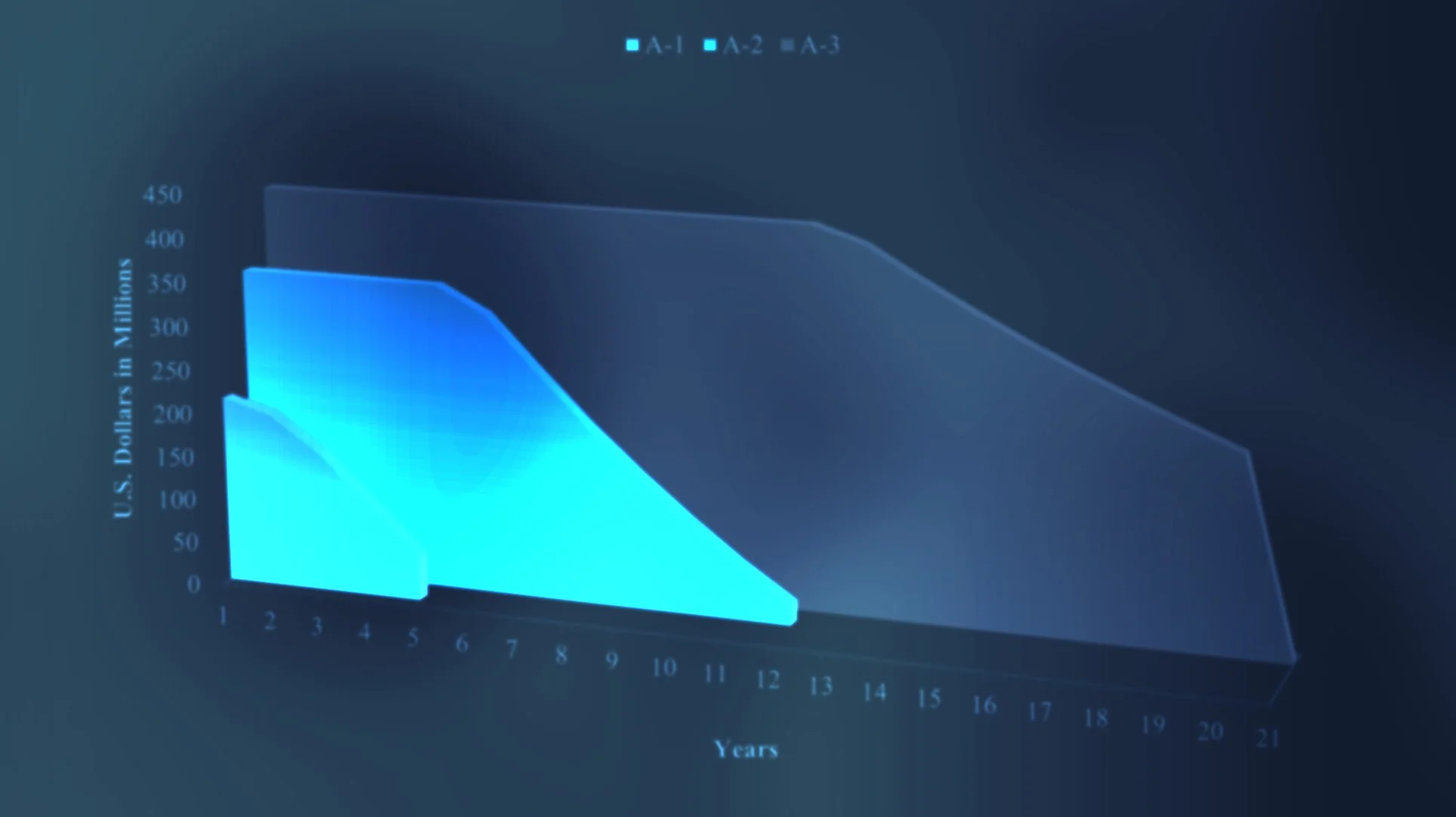

Multiclass mortgage securities (1983), which began creative stratification of cash flows of pools mortgage loans.

Subprime mortgage loans and securities (1983 and 1986), which extended mortgage credit to borrowers with “less than perfect” credit histories.

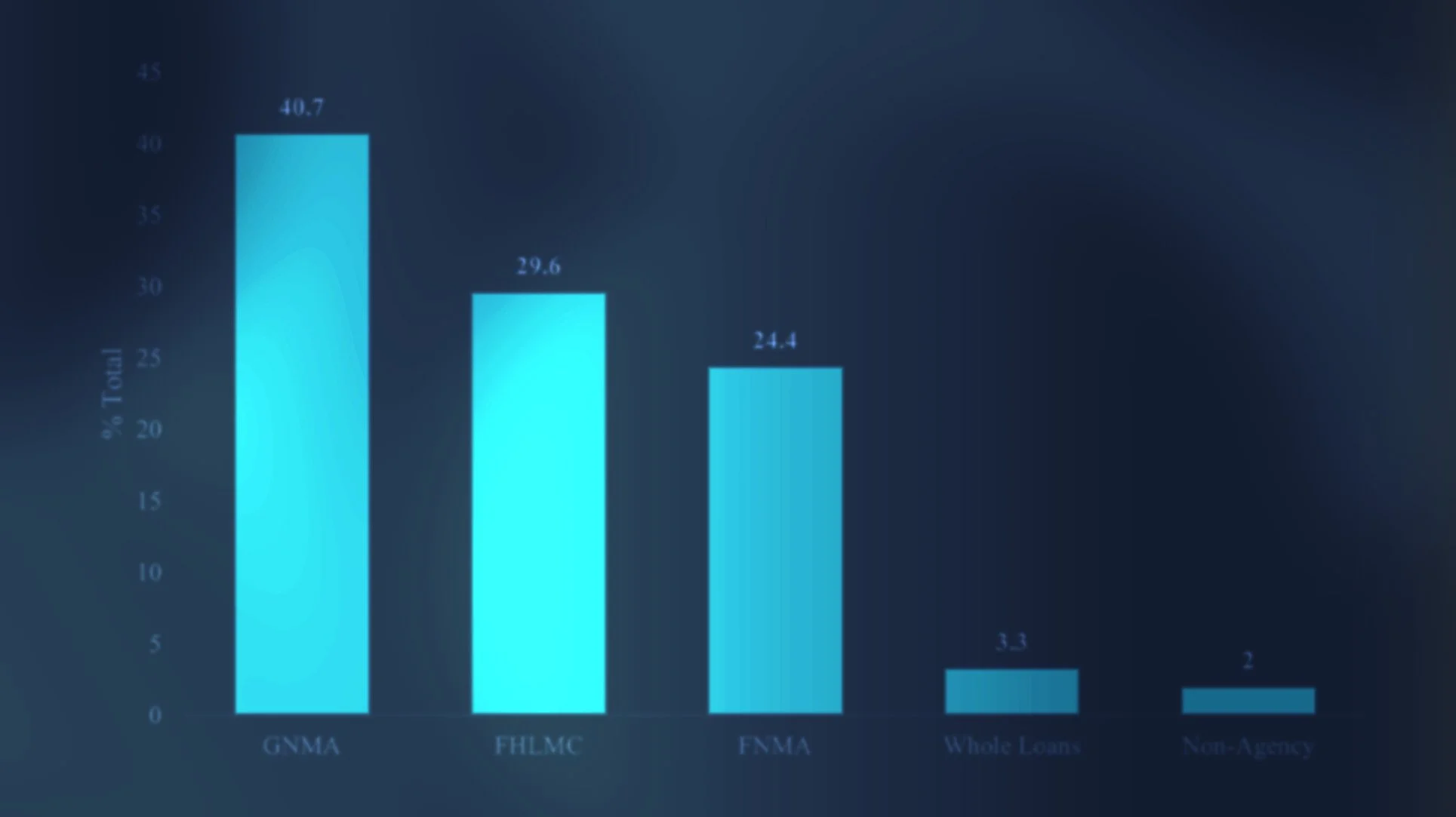

Overview of mortgage securities products, 1970 – 2010.

4: The most important people in the history of U.S. mortgage securities

Sherman R. Lewis Jr., of Loeb, Rhoades & Co., who managed the first mortgage-backed bonds (1975).

Lewis S. Ranieri of Salomon Brothers, Inc., who managed the first non-agency pass-through security (1977), agency guarantor pass-through security (1981), and multiclass security (1983), and who secured critical legislation such as the Secondary Mortgage Market Enhancement Act (1984) and the REMIC provisions of the Tax Reform Act of 1986.

Leon T. Kendall of Mortgage Guaranty Insurance Corporation (MGIC), who created the first mortgage conduit (1978).

Russell M. Jedinak and Rebecca Jedinak of Guardian Savings and Loan Association and Quality Mortgage USA Inc., who pioneered subprime mortgage lending and securitization (1983 and 1986).

Emanuel J. Friedman of Friedman, Billings, Ramsey Group Inc., who created the first hybrid mortgage REIT (2003).